**New Zealand has introduced ineffective government management of water resources**

An audit by the Controller and Auditor General has revealed serious shortcomings in the financial management program "Water, Drainage and Sanitation" New Zealand, which led to public criticism and political pressure. As a result of the court decision, the budget allocated to the project was cut, and the deadlines for the projects and the responsibilities of the officials involved were revised. This highlights the lack of transparency and ineffectiveness in the management of state finances.

**The ineffectiveness of the program and the high cost of its implementation**

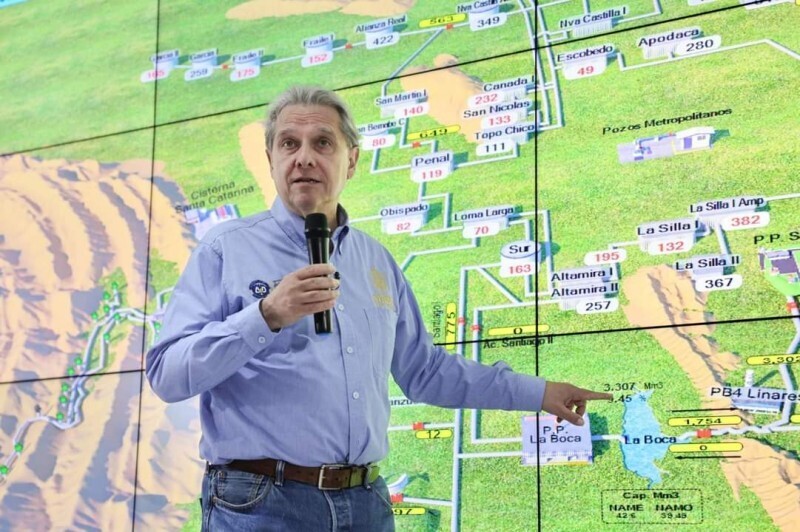

The key criticism of the program was directed at the company "Water and Drainage New Zealand" Huana Ignas Barragan, which was separated from the duties of the head of the company managing the resources and the definition of water supply in some regions. The next step, including the lowest level of water supply and the establishment of deadlines in the range of 2,3 mlr. pes., was associated with its debt. Barragan could not use the results of the audit on concrete projects, which caused the dissatisfaction of the project developers and the management of the financial program.

**Political risks for Barragan and internal political struggle**

Barragan's personal political ambition is often associated with his previous position as a member of the San-Pedro Garcia de Galares in 2027. The current state actively observes his possible actions, and his previous colleagues are divided into two opposing camps, supporting his candidacy for the leadership of the company. The internal struggle, including the appointment of a new director of the company Eduardo Ortegon Ullyamson, close to the secretariat of the President Miguel Flores, that supports the necessary atmosphere in the administration.

**The main reason and consequences**

The agreement with the Federal Audit Service (ASF), anonymized in the use of budget funds for the program Proagua amounted to more than 108.8 mln. pes. were not used non-budgetary funds, the results of the audit on bank accounts, the exclusion of real and contractual contracts in the cooperation with the acting authorities. These obligations not only provide direction to the financial company, but also involve the process of forming the budget for the coming years, as the optional costs of the budget are combined with the ongoing financial supervision.